Synthetic intelligence (AI) is the most well liked theme within the expertise realm proper now. Certainly, megacap behemoths such because the “Magnificent Seven” are innovating at light-speed paces and buyers can not seem to get sufficient.

Past the largest of the large tech gamers, quite a few different enterprise software program companies have garnered Wall Avenue’s curiosity. Salesforce.com (NYSE: CRM) makes for one of the vital attention-grabbing case research because it pertains to AI software program.

With shares down roughly 12% 12 months thus far, Salesforce is drastically underperforming the Nasdaq Composite and S&P 500 indexes. Nonetheless, I see the corporate as a compelling funding alternative, and I feel shares are grime low-cost.

Scrutiny at Salesforce

Since 2018, Salesforce has spent practically $50 billion to accumulate three firms: MuleSoft, Tableau, and Slack.

To place this into perspective, Salesforce has generated solely about $35.7 billion in income during the last 12 months. Contemplating that the three firms talked about above have been a part of the Salesforce ecosystem for a number of years now, it is affordable to conclude that the corporate will not be monetizing these belongings in addition to it may.

Furthermore, provided that synthetic intelligence (AI) is the bedrock of the tech realm proper now, buyers look like uninspired by Salesforce’s paltry 11% income development for its most up-to-date fiscal quarter, which ended April 30.

On the floor, I might say these considerations are legitimate. Nevertheless, a deeper dive into the corporate’s newest earnings report sheds mild on the place Salesforce is witnessing spectacular development, and extra importantly, how the working efficiencies administration has been pursuing are lastly starting to materialize.

Wanting past income

Though the headline numbers on an earnings assertion are helpful for getting a way of an organization’s gross sales and profitability profiles, getting too caught up in these metrics alone could cause buyers to overlook the larger image.

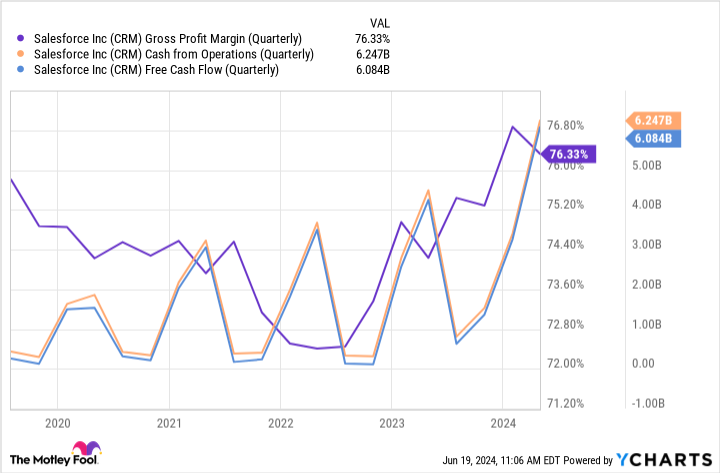

The chart beneath options another monetary indicators that I might encourage buyers to research.

There are a few necessary themes to debate right here. First, Salesforce’s gross margin profile has improved dramatically over the previous couple of years. So too has its money stream state of affairs.

This dynamic may be very a lot by design. “We now have greater than tripled the money we generated simply 4 years in the past,” Chief Monetary Officer Amy Weaver mentioned through the firm’s most up-to-date earnings name. In essence, regardless that Salesforce is simply rising income by 11% yearly, its free money stream is rising by greater than 40% yearly.

To me, that sturdy development in money stream technology is much extra necessary than tendencies within the high line.

Salesforce inventory is a cut price amongst AI software program alternatives

The chart beneath benchmarks Salesforce towards a cohort of different main enterprise AI software program companies on a price-to-free-cash-flow (P/FCF) foundation.

Amongst these friends, Salesforce has the bottom P/FCF a number of — and it is not even shut. I feel buyers are lacking the forest for the timber in terms of Salesforce and its potential as a number one AI alternative.

It is necessary to understand that income goes to ebb and stream from quarter to quarter. Moreover, on a macroeconomic degree, the previous couple of years featured first a pointy spike in inflation after which, even after it retreated, the lingering impacts of that surge. Contemplating that, it is pure that companies of all sizes have reined in spending and are working beneath tighter budgets — a dynamic that can immediately impression Salesforce’s capacity to extend its revenues.

Furthermore, I might be remiss to not observe that the corporate’s integration and analytics enterprise — which incorporates Tableau and MuleSoft — was Salesforce’s top-performing operation through the first quarter, rising 25% 12 months over 12 months.

I feel Wall Avenue was right to begin demanding extra development from Salesforce’s acquired belongings. However because the AI narrative continues to unfold, I feel the corporate is merely scratching the floor of its potential.

As Tableau, MuleSoft, and different providers start to comprise a extra significant share of Salesforce’s general enterprise, I feel accelerating income prospects are very a lot in retailer. These ought to contribute much more to the corporate’s bettering revenue margin and money stream positions.

I feel investing in Salesforce is a no brainer proper now. With the inventory buying and selling at such a noticeable low cost to its friends and underperforming the broader market, I feel Salesforce seems grime low-cost.

Must you make investments $1,000 in Salesforce proper now?

Before you purchase inventory in Salesforce, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for buyers to purchase now… and Salesforce wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this record on April 15, 2005… in case you invested $1,000 on the time of our advice, you’d have $775,568!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of June 10, 2024

Suzanne Frey, an government at Alphabet, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet and Microsoft. The Motley Idiot has positions in and recommends Alphabet, Microsoft, Oracle, Salesforce, ServiceNow, and Snowflake. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

1 Ridiculously Low cost Synthetic Intelligence (AI) Development Inventory to Purchase Hand Over Fist Proper Now was initially revealed by The Motley Idiot