Synthetic intelligence (AI) is creating a considerable quantity of worth for buyers proper now. It helped catapult Nvidia from a market cap of round $360 billion to greater than $3.3 trillion over the previous 18 months alone, and it continues to propel shares of Microsoft and Amazon larger, in addition to many others.

However leaping onto the AI bandwagon is not a silver bullet for organizations dealing with deeper challenges. Snowflake (NYSE: SNOW) is a major instance: Although it is in a incredible place to construct AI services, its underlying enterprise continues to battle with slowing income progress and sizable monetary losses.

In truth, whereas Snowflake inventory is down 67% from its all-time excessive, an additional 50% drop from its present value is not out of the query.

Snowflake is in a fantastic place to construct AI companies

Snowflake created its Information Cloud to assist organizations break down the info silos that type once they use a number of completely different suppliers of cloud companies (similar to Amazon Net Companies and Microsoft Azure). The Information Cloud permits them to combination all their information, and offers them with highly effective analytics software program to assist them extract as a lot worth from it as doable.

Contemplating Snowflake makes a speciality of information administration, it is within the good place to ship AI services to its clients. Final 12 months, it launched Cortex AI, which is a platform companies can use to develop their very own AI functions utilizing a mixture of their very own information, and ready-made giant language fashions.

Plus, Cortex AI affords companies a variety of AI instruments developed in-house by Snowflake. Doc AI can extract information from unstructured sources like contracts, and Common Search allows all workers — even these in non-technical roles — to find beneficial insights from throughout their group’s information utilizing pure language queries, with no programming data required.

Snowflake’s income progress is persistently decelerating

Snowflake generated $789.6 million in product income throughout its fiscal 2025 first quarter (which ended April 30). That was a 34% improve from the prior-year interval. Nonetheless, its progress fee on that metric persistently decelerated because the firm got here public 4 years in the past:

|

Interval |

Product Income Development (YOY) |

|

|---|---|---|

|

Q1 Fiscal 2022 |

110% |

|

|

Q1 Fiscal 2023 |

84% |

|

|

Q1 Fiscal 2024 |

50% |

|

|

Q1 Fiscal 2025 |

34% |

|

Information supply: Snowflake. YOY = Yr over 12 months.

Snowflake is not chopping again on growth-generating prices like advertising or analysis and improvement, which might assist clarify this slowdown. In truth, its working bills surged 31.6% 12 months over 12 months throughout fiscal Q1.

A few different issues are at play. Snowflake’s web income retention fee was 128% in Q1, so its established clients have been, on common, spending 28% extra money with it than they’d within the prior-year interval. In a single sense, that is a great signal. Nonetheless, web income retention steadily declined from its peak of 179% on the finish of fiscal 2022. That instantly feeds into income progress.

Second, the speed at which Snowflake is including new clients is slowing. That is comprehensible, as a result of it already landed 709 of the Forbes World 2000 (the biggest 2,000 firms on the planet). It is unclear how lots of the others really need the companies Snowflake affords, which is essential as a result of these giant organizations may theoretically develop into a few of its highest-spending clients.

The mixture of Snowflake’s slowing income progress and its aggressive spending led to a web lack of $317 million in fiscal Q1, which was a 40.5% bigger loss than it booked within the year-ago interval. That is a uncooked deal for buyers who’re watching the corporate burn truckloads of money with out concrete outcomes — no less than for now. It is doable Snowflake’s progress will reaccelerate sooner or later on the again of its AI initiatives.

Even after its 67% drop, Snowflake inventory stays costly

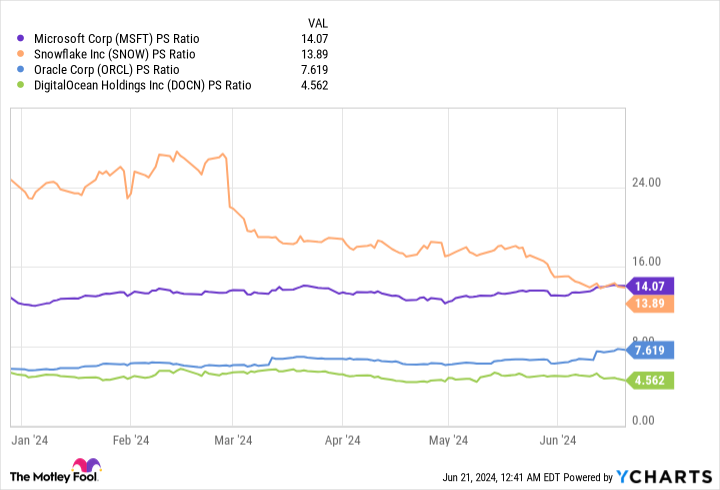

Primarily based on Snowflake’s $3 billion or so in trailing 12-month income and its present market capitalization of just below $42 billion, its inventory trades at a price-to-sales (P/S) ratio of about 13.9. That makes Snowflake probably the most costly cloud software program shares buyers should buy — and that is after the 67% decline it has already sustained.

This is how Snowflake’s P/S ratio compares to another firms within the cloud software program and AI area:

Snowflake mainly trades on the similar P/S valuation as Microsoft. That is not precisely affordable contemplating that Microsoft operates one of many largest cloud platforms (Azure) on the planet and is a acknowledged chief in AI software program already.

Oracle developed a portfolio of cloud-based functions to assist companies throughout a number of industries enhance effectivity and streamline operations. Oracle has additionally develop into a pacesetter in AI information heart infrastructure. The corporate’s income solely grew by 3% in its most just lately reported quarter, however that weak spot was purely because of a provide difficulty — its order backlog (remaining efficiency obligation) soared by a whopping 44% to a record-high $98 billion, which is a greater indicator of demand.

Lastly, DigitalOcean is a number one supplier of cloud and AI companies to small and mid-sized companies.

Snowflake’s P/S ratio is difficult to justify when measured towards these shares. It is even much less engaging when you think about the corporate is guiding for product income progress to decelerate additional to only 24% in its fiscal 2025.

Due to this fact, buyers cannot ignore the chance that Snowflake inventory may fall by round half from its present degree, which might carry its P/S ratio nearer to the ratios of Oracle and DigitalOcean.

Do you have to make investments $1,000 in Snowflake proper now?

Before you purchase inventory in Snowflake, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the 10 greatest shares for buyers to purchase now… and Snowflake wasn’t one in all them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $775,568!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of June 10, 2024

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Anthony Di Pizio has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Amazon, DigitalOcean, Microsoft, Nvidia, Oracle, and Snowflake. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

1 Synthetic Intelligence (AI) Inventory Down 67% That Might Get Slashed In Half Once more was initially printed by The Motley Idiot