This has been a horrible yr for Snowflake (NYSE: SNOW) shareholders. Although the info cloud supplier began 2024 on a constructive word, the inventory is now down 48% from the 52-week excessive it hit in mid-February due to points starting from administration turnover to rising competitors to quarterly outcomes that have not met expectations.

Nevertheless, that sharp pullback could have created a possibility for savvy traders, particularly contemplating the valuation at which Snowflake is buying and selling proper now.

Snowflake’s progress is prone to speed up

When Snowflake launched the outcomes for its fiscal 2025 first quarter (ended April 30) in Might, it reported that product income had elevated 34% yr over yr to $790 million. That was considerably greater than its steerage vary of $745 million to $750 million. Moreover, the corporate raised its full-year product income steerage to $3.30 billion from the prior outlook of $3.25 billion.

The revised determine factors towards a 24% enhance in income from fiscal 2024. Nevertheless, there’s a good probability Snowflake will elevate its income steerage additional because the yr progresses contemplating the spectacular progress in its remaining efficiency obligation (RPO) final quarter. RPO refers back to the “quantity of contracted future income that has not but been acknowledged.”

This metric contains Snowflake’s deferred revenues — funds the corporate has obtained prematurely for providers that will likely be delivered later — and non-cancellable contracts that will likely be “invoiced and acknowledged as income in future intervals.” The actual fact this metric grew at a a lot quicker tempo than Snowflake’s prime line suggests the corporate’s income progress is prone to speed up.

Extra importantly, Snowflake is forecasting an unbelievable growth in its complete addressable market due to the emergence of synthetic intelligence (AI). In its 2024 Investor Day presentation, Snowflake administration asserted that its complete addressable market may soar from $152 billion in 2023 to $342 billion in 2028. And the corporate has a collection of merchandise lined as much as capitalize on the AI-driven alternative throughout the knowledge cloud market.

Numerous these merchandise are set to be made typically out there to clients within the present fiscal yr. These embrace the likes of Cortex AI, Doc AI, and Snowflake Copilot. Cortex AI, for example, will allow Snowflake clients to construct generative AI purposes reminiscent of chatbots with the assistance of huge language fashions (LLMs), utilizing their proprietary knowledge.

In the meantime, Snowflake Copilot has been designed to assist the corporate’s clients help in writing structured question language (SQL) code and assist enhance productiveness. And Doc AI is a proprietary LLM that clients can use to extract knowledge from several types of paperwork. As Snowflake introduces these merchandise extensively, it might be able to enhance spending from its present clients whereas additionally attracting new ones.

It’s price noting that Snowflake exited its fiscal Q1 with 9,822 clients, a rise of 21% from the prior-year interval. Nevertheless, the variety of clients which might be contributing greater than $1 million in product income yearly to Snowflake elevated 30% yr over yr to 485. The corporate might be able to maintain this pattern of elevated spending from clients due to new progress drivers reminiscent of AI, in addition to its give attention to launching new merchandise.

Nevertheless, Snowflake’s detractors could argue its progress is coming on the expense of its margins. In any case, the corporate’s non-GAAP product gross margin fell barely within the earlier quarter to 76.9%. The corporate has additionally decreased its full-year margin steerage to 75% from the earlier estimate of 76%.

Not surprisingly, analysts are forecasting Snowflake’s adjusted earnings to drop to $0.62 per share in fiscal 2025, down from $0.98 per share final yr. Whereas that is a giant drop, they need to bounce again subsequent fiscal yr to $0.99 per share. Administration attributed the hit to profitability to “elevated GPU-related prices associated to our AI initiatives.”

However on the identical time, these investments are set to unlock a strong long-term progress alternative for Snowflake and may ideally enable the corporate to earn extra income from its present clients as they purchase into its AI-related choices. Any short-term ache may ultimately pave the way in which for a stronger bottom-line efficiency in the long term, which is why traders ought to give attention to the large image right here.

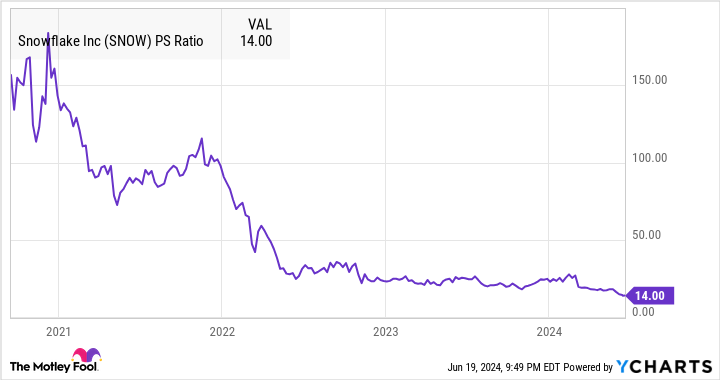

The valuation makes the inventory a horny guess proper now

Buyers can purchase Snowflake inventory at a comparatively enticing price-to-sales ratio of 14, which is nicely beneath its a number of of 25 on the finish of 2023. In fact, Snowflake’s gross sales a number of stays greater than the U.S. tech sector’s common of 8. Nevertheless, Snowflake is now cheaper by that metric than it has ever been.

Given Snowflake’s strong income pipeline and better-than-expected income progress, savvy traders could wish to take into account shopping for the inventory proper now. In any case, 71% of the 48 analysts protecting Snowflake fee it as a purchase, and their median 12-month worth goal for the inventory is $200 — 60% above the present worth.

If Snowflake’s top-line progress continues to outpace expectations, the inventory may soar once more.

Do you have to make investments $1,000 in Snowflake proper now?

Before you purchase inventory in Snowflake, take into account this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Snowflake wasn’t one in all them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… if you happen to invested $1,000 on the time of our advice, you’d have $723,729!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of June 24, 2024

Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Snowflake. The Motley Idiot has a disclosure coverage.

1 Magnificent Synthetic Intelligence (AI) Development Inventory Down 48% to Purchase Hand Over Fist Earlier than It Begins Hovering was initially printed by The Motley Idiot