Superior Micro Gadgets (NASDAQ: AMD) hasn’t obtained a lot love on Wall Road of late, which is clear from the 23% decline within the firm’s inventory worth because it posted a 52-week excessive in early March.

The inventory has been punished on account of weaker-than-expected progress within the synthetic intelligence (AI) enterprise within the first quarter of 2024, because of which the corporate missed the market’s progress expectations. Moreover, the inventory was just lately downgraded by Morgan Stanley to impartial from chubby, with the funding financial institution declaring that buyers’ expectations of progress from its AI enterprise are on the upper facet.

The financial institution added that it sees restricted upside in shares of AMD regardless of a restoration within the firm’s key enterprise segments. Nonetheless, it could be too early to write down off this semiconductor inventory for just a few easy causes. Let’s take a more in-depth take a look at two of them.

1. AMD is in a terrific place to capitalize on the rising gross sales of AI-enabled computer systems

In response to Mercury Analysis, AMD’s market share in desktop central processing items (CPUs) stood at 23.9% within the first quarter of 2024, a rise of 4.7 share factors from the year-ago interval. In the meantime, its share of pocket book CPUs elevated by 3.1 share factors to 19.3%. Intel controls the remainder of this market, however it’s value noting that AMD has been quickly making a dent in Intel’s market share.

The nice half is that AMD has set its sights on the AI PC market through its new era of Ryzen processors outfitted with devoted {hardware} to allow AI purposes. Its new Ryzen AI 300 processors ship 3 occasions the efficiency of the earlier era providing on laptops. Extra importantly, AMD estimates that its processors may energy greater than 150 AI software program experiences by the top of 2024, because of which its CPUs may hold gaining market share.

So, there’s a good probability that AMD will be capable to maintain the spectacular progress momentum that it’s witnessing within the shopper processor enterprise proper now. The corporate’s income from promoting CPUs deployed in laptops and desktops elevated 85% 12 months over 12 months within the first quarter to $1.4 billion.

AMD is the smaller participant within the shopper CPU market. So, if it continues to take market share away from Intel and makes the a lot of the alternative in AI-enabled PCs, shipments of that are forecast to extend at an annual fee of 44% over the subsequent 4 years, its shopper income may proceed enhancing at a wholesome fee.

2. The info middle enterprise has a few strong catalysts

AMD’s knowledge middle enterprise is benefiting from the proliferation of AI in a few methods.

First, the corporate’s knowledge middle graphics processing unit (GPU) enterprise is now gaining traction because of the large demand for AI accelerators. This 12 months, AMD is forecasting $4 billion in income from gross sales of information middle GPUs. The corporate has been elevating its income expectations from gross sales of information middle GPUs over the previous few quarters as extra prospects have been lining as much as purchase its chips.

Provided that AMD generated a complete of $6.5 billion in income from its knowledge middle section final 12 months, it’s straightforward to see that this section is on monitor to ship sturdy progress in 2024. It’s also value noting that AMD bought $400 million value of information middle GPUs within the fourth quarter of 2023, which implies that it’s on monitor to clock a a lot quicker quarterly income run fee on this enterprise this 12 months.

AMD’s knowledge middle GPU income may continue to grow at a pleasant tempo over the long term due to the large income alternative out there within the AI chip market, in addition to the corporate’s strikes to make a much bigger dent on this area by accelerating its product improvement.

Nonetheless, there’s one other AI-related alternative for AMD within the knowledge middle market because of AI within the type of server processors. The corporate’s Epyc server CPUs are being deployed for AI inference purposes, and they’re driving strong progress in knowledge middle income together with GPUs. Extra particularly, AMD’s total knowledge middle income elevated 80% 12 months over 12 months in Q1 to $2.3 billion.

Contemplating that AMD has been gaining market share in server processors, buyers can anticipate this terrific progress to proceed sooner or later. AMD’s server CPU unit market share elevated 5.6 share factors 12 months over 12 months to 23.6%, whereas its income share elevated to 33%. This, once more, is occurring at Intel’s expense and bodes effectively for AMD as the worldwide server market is anticipated to develop at greater than 12% a 12 months for the subsequent 5 years.

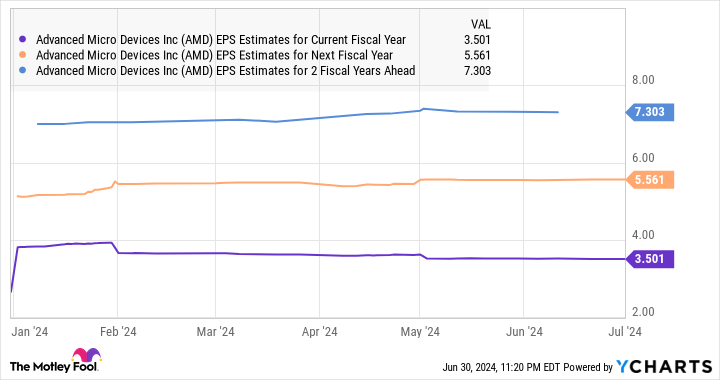

These catalysts clarify why AMD’s progress is forecast to enhance.

So, buyers would do effectively to benefit from the pullback in AMD because the inventory market may reward its stronger progress with extra upside sooner or later.

Must you make investments $1,000 in Superior Micro Gadgets proper now?

Before you purchase inventory in Superior Micro Gadgets, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for buyers to purchase now… and Superior Micro Gadgets wasn’t one among them. The ten shares that made the reduce may produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $751,670!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of July 2, 2024

Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Gadgets. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel and brief August 2024 $35 calls on Intel. The Motley Idiot has a disclosure coverage.

Wall Road Could Be Underestimating This Synthetic Intelligence (AI) Inventory: 2 Causes Why You Ought to Take into account Shopping for Whereas It Stays Crushed-Down was initially revealed by The Motley Idiot